1/2

North America Doors Market Size, Share & Growth, 2033

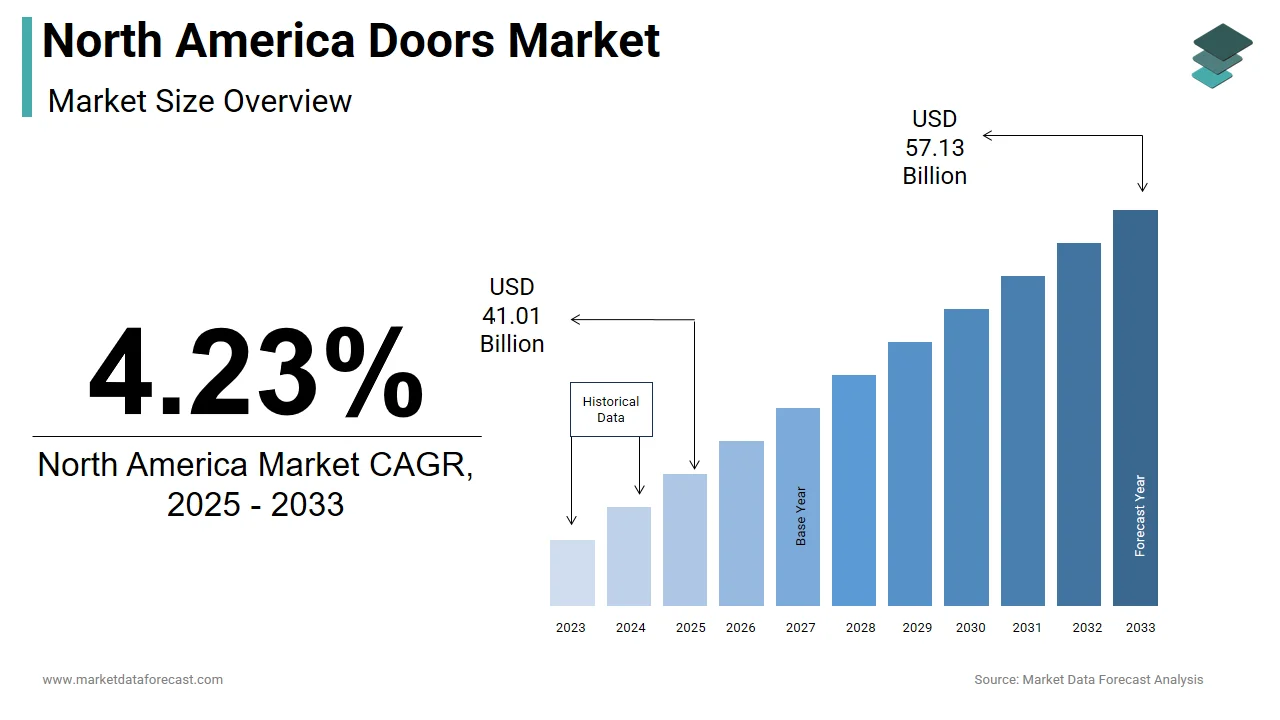

The North America doors market, valued at USD 39.35 billion in 2024, is projected to reach USD 57.13 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 4.23% from 2025 to 2033. This market encompasses a diverse range of interior and exterior doors for residential, commercial, and industrial applications, manufactured from materials such as wood, steel, aluminum, fiberglass, and composites. Key market drivers include the robust growth in residential construction and home renovation activities across North America. For instance, the U.S. Census Bureau reported approximately 1.47 million housing completions in 2023, significantly boosting demand for doors. Homeowners are increasingly investing in premium, energy-efficient, and technologically advanced door solutions to enhance aesthetics, thermal performance, and security. The rising demand for energy-efficient and sustainable door products also fuels market expansion, driven by environmental awareness and stringent regulatory frameworks. Manufacturers are responding with insulated core doors, weather-stripped frames, and high-performance glazing options, alongside the adoption of certified sustainable wood doors in public infrastructure projects.

However, the market faces significant restraints, including supply chain disruptions and raw material price volatility. The cost of essential materials like wood, steel, aluminum, PVC, and glass has fluctuated due to global economic uncertainties, impacting profit margins and leading to higher retail prices. Supply chain bottlenecks, exacerbated by labor shortages and transportation backlogs, have caused delays in raw material reception for 72% of door manufacturing firms in 2023, according to the Institute for Supply Management. Another major challenge is the labor shortage in construction and installation sectors, particularly for skilled professionals like carpenters and installers. The Associated General Contractors of America reported that 89% of U.S. construction firms struggled to hire qualified door installers in 2023, leading to project delays and increased labor costs.

Despite these challenges, significant opportunities exist within the market, particularly with the expansion of smart and connected door technologies. Innovations such as motorized entry systems, biometric locks, and integration with home automation platforms are gaining traction in both residential and commercial sectors, driven by heightened security concerns and the proliferation of smart home ecosystems. The growth of e-commerce and direct-to-consumer (DTC) sales channels also presents a lucrative opportunity. Online platforms offer convenience, virtual visualization tools, and augmented reality integrations, catering to changing consumer behaviors and allowing major brands to expand their digital presence.

Intense competition and price sensitivity among consumers pose a continuous challenge, with many prioritizing cost over brand reputation or sustainability. This has led to aggressive pricing strategies and increased demand for cost-effective alternatives. Furthermore, regulatory compliance and environmental standards, particularly regarding emissions and indoor air quality, require manufacturers to invest in compliant materials and testing procedures. Smaller manufacturers, in particular, face difficulties adapting to evolving regulations without compromising profitability.

Segmental analysis reveals that wood doors held the largest material share at 35.4% in 2024, owing to their aesthetics, durability, and customization options, while composite doors are the fastest-growing segment, driven by demand for strength, thermal efficiency, and low maintenance. Swinging doors dominate the mechanism segment with 48.2% of the market due to their simplicity and widespread use, while folding doors are the fastest-growing, reflecting trends in open-space living. Interior doors account for the largest product type share at 54.1%, being essential for every structure, and exterior doors are the fastest-growing, fueled by focus on security and energy efficiency. New construction represents the largest mode of application at 61.4%, supported by residential and commercial building activities, while the aftermarket segment is the fastest-growing, driven by home improvement and retrofitting activities. The United States holds the largest share of the North America doors market, followed by Canada and Mexico. Key market players, including Masonite, JELD-WEN, and Therma-Tru, are focused on product innovation, vertical integration, and digital transformation to maintain competitiveness.

#NorthAmericaDoorsMarket #ResidentialConstruction #HomeRenovation #EnergyEfficientDoors #SmartDoorTechnologies #SupplyChainDisruptions #RawMaterialPrices #LaborShortages #ECommerceGrowth #SustainableBuilding #NorthAmericaDoorsMarket #ResidentialConstruction #HomeRenovation #EnergyEfficientDoors #SmartDoorTechnologies #SupplyChainDisruptions #RawMaterialPrices #LaborShortages #ECommerceGrowth #SustainableBuilding

0 comment in total

You may also like

![Doors Market, Industry Size Growth Forecast Report, [Latest]](https://gstatic.ideal.house/news/images/49bdcee660bd4d108750313d21923184.webp)

Doors Market, Industry Size Growth Forecast Report, [Latest]

North America Smart Lighting Market Size

Interior Design Market Size and Forecast (2025–2033): A Rising Global Demand for Smart, Sustainable, and Personalized Spaces

Top 10 Door Manufacturing Companies in India

Curtain Wall Market | Global Market Analysis Report - 2035

Embracing Style and Functionality: Interior Door Hardware Trends of 2025

Europe Gypsum Board Market Size, Share and Analysis, 2033

Q + A with Roto Frank North America | Innovative Solutions Shaping the Future

Remodeling Market Size, 2025-2034 Trends Report

Global Plywood Market Size and Forecast 2025–2033

Bathroom Cabinets Market Size, Share | CAGR of 6.3%

Designers Agree: Homeowners Want This Design Feature in 2026 (For Every Room!)

North America Garage Overhead Doors Market Size, Share, 2033

Linen Market Size, Share, Trends & Growth Report, 2033

Global Carpet Market Size and Forecast 2025–2033

![Modular Flooring Market Size & Forecast [Latest]](https://gstatic.ideal.house/news/images/88e7dffc81964dc0b0928f6aca821eed.jpg)

Modular Flooring Market Size & Forecast [Latest]

Drive Profitability with These 3 Emerging Door Trends

Modular Kitchen Market Size, Share, Demand | CAGR of 5.3%