FHA 203(k) Loan: Renovation Mortgage Guidelines

An FHA 203(k) loan is a specialized mortgage product that allows homeowners and homebuyers to finance both the purchase or refinancing of a home and the costs of its renovation or repair into a single loan. This type of loan is insured by the Federal Housing Administration (FHA), which results in more flexible qualification requirements compared to conventional renovation loans, making it accessible to a wider range of borrowers, particularly those with less-than-perfect credit scores or lower down payments.

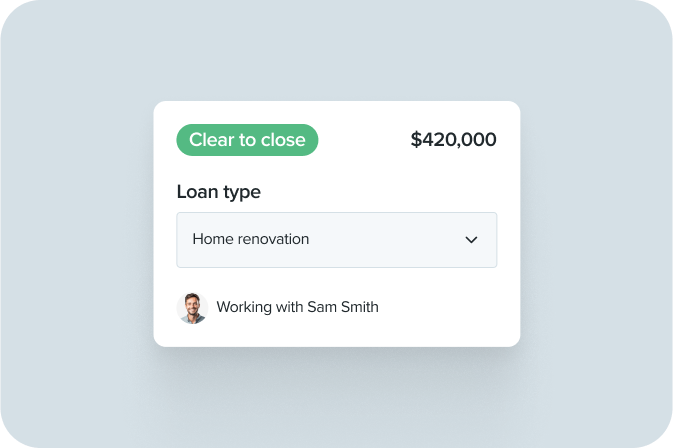

There are two primary types of FHA 203(k) loans: the limited (or streamline) 203(k) and the standard 203(k). The limited 203(k) loan is designed for homes that require moderate repairs or cosmetic upgrades, with a typical borrowing limit of up to $75,000 for renovations. This option is suitable for projects such as updating kitchens or bathrooms, replacing flooring, or making FHA-required repairs, but it does not permit major structural changes. In contrast, the standard 203(k) loan is intended for more extensive renovation projects, including major structural work, and requires a minimum draw of $5,000 for renovations. This type of loan can even cover full demolition and reconstruction, provided the original foundation remains intact. Due to the complexity of these projects, a standard 203(k) loan necessitates the involvement of an FHA-approved consultant, typically with backgrounds in engineering or architecture, to oversee the renovations.

FHA 203(k) loans can be utilized for various improvements, such as enhancing a home’s functionality or attractiveness, addressing health and safety hazards, upgrading plumbing or sewer systems, installing or repairing roofs and gutters, replacing flooring, improving landscaping, ensuring accessibility for disabled individuals, or making a home more energy-efficient. All renovations funded by a 203(k) loan must generally be performed by a licensed contractor and are subject to FHA appraiser approval and, for standard loans, consultant oversight. The renovation work must commence within 30 days of closing and be finalized within six months. If the home becomes uninhabitable during the renovation period, a portion of the loan funds can be allocated to cover mortgage payments.

Qualification for an FHA 203(k) loan aligns with general FHA mortgage requirements. This includes a minimum credit score of 500, although some lenders may impose higher minimums. A down payment of 3.5% is required for credit scores of 580 or higher, while those with scores between 500 and 579 must provide a 10% down payment. FHA loan limits, which vary by location, also apply to 203(k) loans, capping the maximum loan amount. Generally, a foreclosure within the past three years disqualifies an applicant. These loans also require FHA mortgage insurance. Borrowers interested in a 203(k) loan must seek an FHA-approved lender and provide documentation for income, debts, and credit score. While FHA loans often have lower closing costs than conventional mortgages, additional origination fees and higher appraisal fees may apply.

#FHALoan #HomeRenovation #MortgageFinancing #RealEstate #HomeImprovement #PropertyValue #CreditScore #HousingMarket #GovernmentBackedLoan #FHALoan #HomeRenovation #MortgageFinancing #RealEstate #HomeImprovement #PropertyValue #CreditScore #HousingMarket #GovernmentBackedLoan

0 comment in total

You may also like

How to create your own dream home: home renovation trends

Renovation

Renovation of the Year

What Happens If I Don’t Get a Permit for My Home Remodel?

Home renovation loan benefits & guidelines

You should try to avoid these 10 common home remodeling mistakes, urge experts

A beginner’s guide to home remodeling: 5 rules to follow

Renovate | Build

Fine Homebuilding Online Archive

Amaral Services General Contracting shares tips on Home Remodeling Projects

6 Renovating Myths I Uncovered While Getting My General Contractor’s License

We’re Calling It: This Is the Year for a Kitchen Renovation

What are the hottest home renovations for the summer?

9 Things You Need to Know Before Renovating Your Home, According to Experts

Home Renovation Ideas - How To Renovate a House

Kitchen Renovation Tips HGTV's Hilary Farr Swears By

Planning a kitchen: The ultimate guide to renovation and installation

Remodeling

This Kitchen Renovation Timeline Will Help Guide Your Project in 2026

6 Headache-Saving Tips You Should Know Before Starting a Remodel, According to Designers