Ceramic Update: As duties on Chinese tile necessitate a sourcing shift in the U.S. market, who will fill the gap? - March 2020

The ceramic tile industry, a long-established sector, is currently navigating significant challenges, primarily stemming from substantial duties imposed on Chinese imports and the rapid ascent of Luxury Vinyl Tile (LVT) in the hard surface flooring market. These factors have spurred innovation and diversification within the ceramic industry to address hurdles such as labor shortages and shifting consumer preferences. The U.S. ceramic tile market experienced a 2% revenue dip in 2019, closing at $3.4 billion, with imports falling by an estimated 2.7% to $2.1 billion during the same period.

The trade war initiated by the Trump administration led to a 10% tariff on $200 billion worth of Chinese imports, including flooring, in September 2018. This tariff incrementally increased over 18 months, reaching 35% on ceramic imports from China. Further exacerbating the situation, the U.S. Commerce Department imposed countervailing duties ranging from 104% to 222% in September 2019, targeting Chinese tile imports valued at approximately $483.1 million in 2018. These duties, particularly the requirement for upfront payment, have effectively eliminated Chinese ceramic tile imports, which previously constituted about one-third of the U.S. market by value. This creates a significant gap of approximately 700 million square feet of product that needs to be filled.

While this presents an opportunity for domestic manufacturers, filling this void is not straightforward. U.S. manufacturers may not be operating at full capacity, and expanding production takes time. Establishing new relationships and securing orders are crucial steps for domestic entities to capitalize on this shift. Some U.S. producers, like Crossville and Florida Tile, have seen moderate increases in sales due to China's reduced presence, emphasizing the importance of a strong domestic supply base. However, distributors who previously relied on Chinese imports, such as MSI Surfaces and Emser, express concerns about the negative impact on product availability, consumer choice, and potential price increases, especially for specialized tile types. U.S. capacity alone is insufficient to meet the demand, with estimates suggesting only 200 million square feet could be added by maximizing domestic production. This shortfall is predicted to lead to higher prices and a potential shift towards LVT and other materials.

To manage the shift, companies are diversifying their product offerings and seeking suppliers from non-tariffed countries like India, Turkey, and Brazil. The market is also undergoing channel changes, with major players like Daltile and Crossville establishing direct-to-end-user retail centers, which streamline the distribution process and offer direct customer engagement. This trend, coupled with the rise of private-label products, is flattening the market and challenging traditional distribution models. Effective strategies in this evolving market involve specialization and strong communication between distributors and manufacturers to address market needs.

A significant aspect of the ceramic industry's current landscape is its competition with LVT, particularly regarding waterproof claims. Ceramic manufacturers assert that only ceramic offers a truly waterproof installation, as LVT's groutless nature can allow moisture seepage, fostering mold and mildew. Studies by Clemson University, commissioned by the Tile Council of North America (TCNA), found that most LVT products tested supported mold growth, despite claims of being waterproof, and their warranties often disclaimed damage from mold. This highlights a discrepancy between consumer perception and the reality of LVT performance. The ceramic industry is advocating for a clear, industry-wide educational campaign to differentiate ceramic's advantages in durability, sustainability, and true waterproof capabilities. This long-term strategy aims to counter LVT's marketing prowess and re-educate consumers, potentially leading to an upgrade from LVT to ceramic over time.

Furthermore, innovations in installation systems are addressing labor shortages and making ceramic tile more accessible. Daltile's RevoTile, a click-together system, simplifies installation with its selection of popular visuals. Other systems like Drytiling and Ceraclick also aim to speed up installation. While these systems simplify the process, proper subfloor preparation remains critical. The potential for DIY and less experienced installers to use these systems could significantly expand the ceramic market, particularly if cost savings are passed on to consumers. These innovations, combined with the expansion of ceramic applications beyond traditional uses, indicate a dynamic industry striving to adapt and grow amidst market shifts and competitive pressures.

#CeramicTile #TradeDuties #USMarket #SourcingShift #LVTCompetition #InstallationInnovation #WaterproofFlooring #DomesticManufacturing #SupplyChain #CeramicTile #TradeDuties #USMarket #SourcingShift #LVTCompetition #InstallationInnovation #WaterproofFlooring #DomesticManufacturing #SupplyChain

0 comment in total

You may also like

Reliable companies to consider when looking to buy tiles

Discover The Top 10 Tile Trends Discusses at Coverings 2025

How Spain’s Decocer is taking quality ceramic fashion global

Top 10 Ceramic Tiles Manufacturing Companies In India

Ceramics of Italy predicts tile trends for 2019

Miles of Tile at Cersaie 2022

USA Tile And Marble Offers Selection, Value, Experience

Hardwood Report 2025: The hardwood industry continues to improve its offering – March 2025

Delftware porcelain – the global story of a Dutch icon

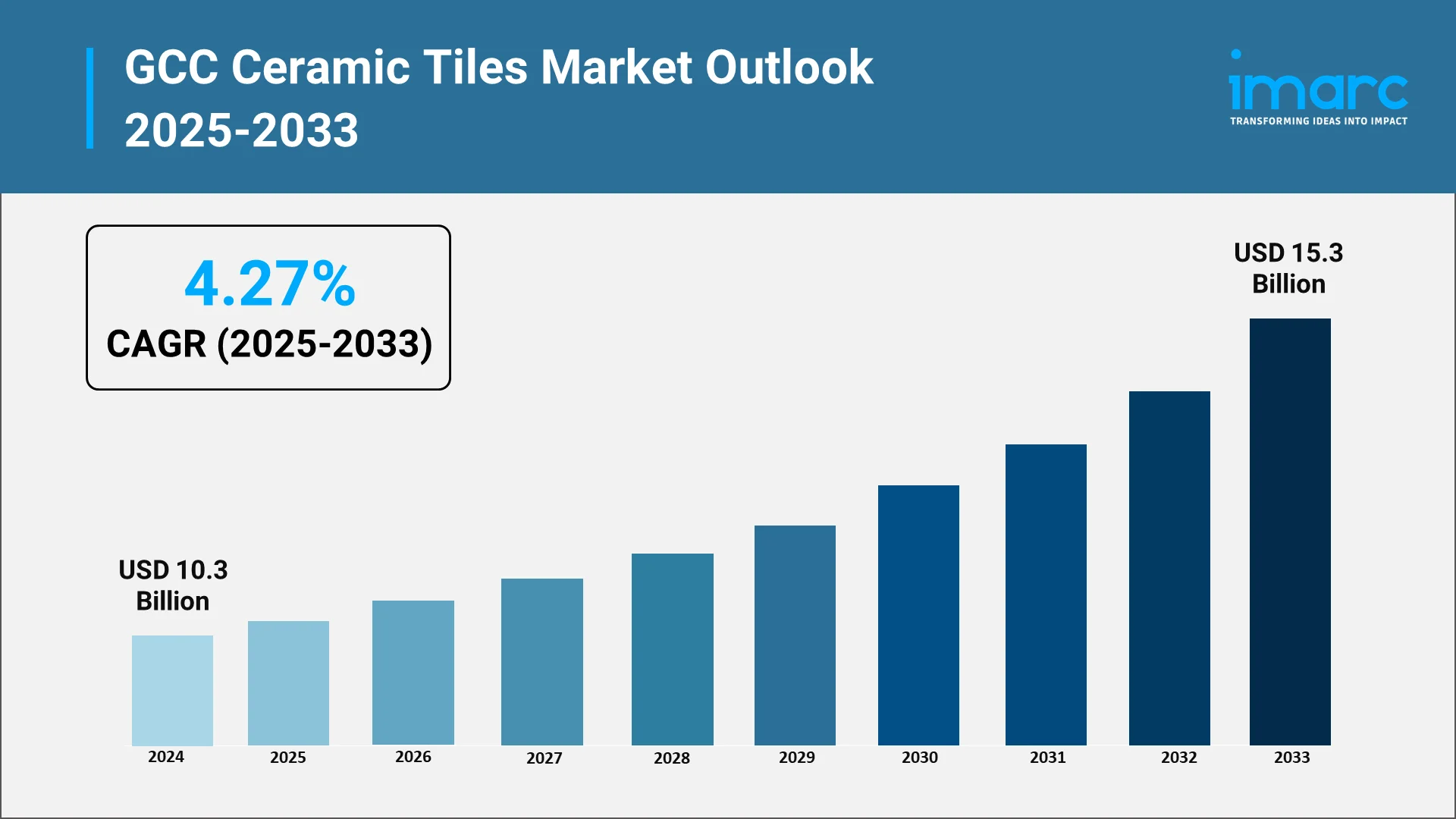

GCC Ceramic Tiles Market Grows with Rising Construction Demand

Orient Ceramics & Industries Limited Long Term Buy Call : Fairwealth Securities

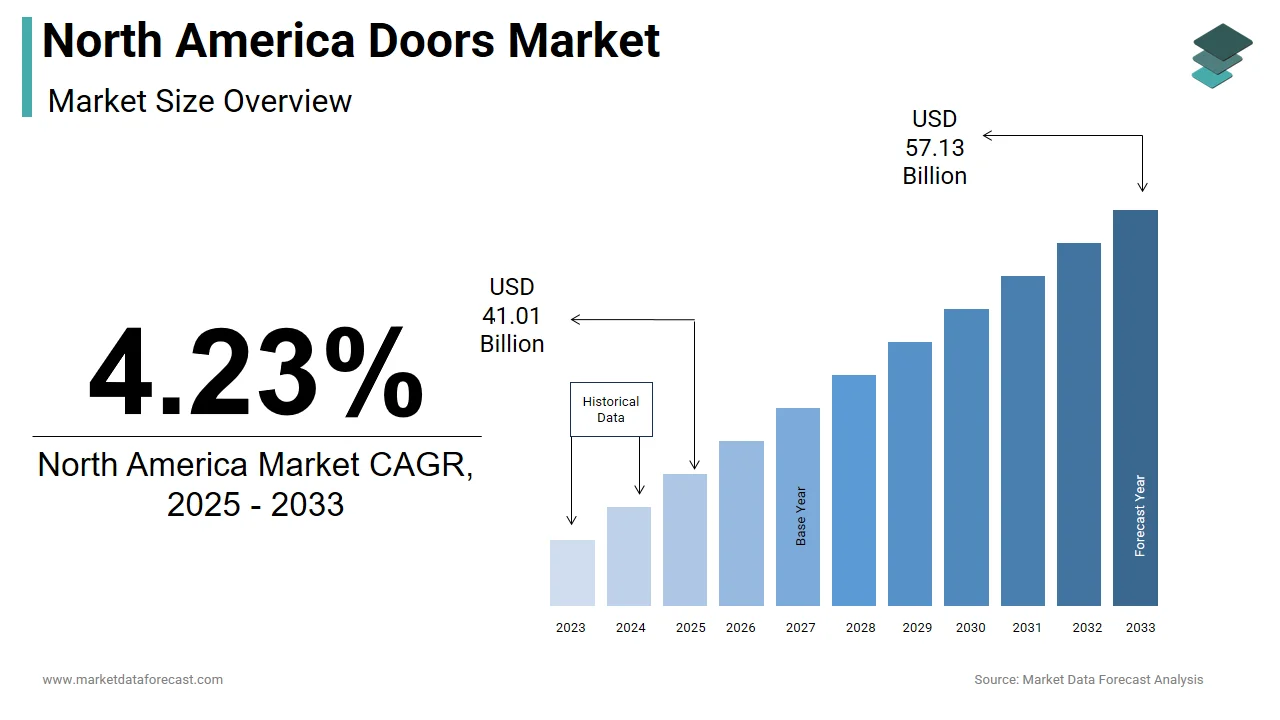

North America Doors Market Size, Share & Growth, 2033

Ceramic Tile Report: Tariffs put renewed focus on domestic supply – April 2025

The New Tile Trend Causing a Scene This Season

How Tariffs Will Impact Your Next Home Improvement Project

These Are the Home Products That Could Be Impacted by Tariffs—Plus How to Save

7 Top Tile Trends And Styles For 2021

World Of Tiles Reveal This Year's Tile & Wood Flooring Trends

Best Tile Manufacturers and Tile Brands

Key Players in the Flooring Market